How long does a home equity loan take? This question is at the forefront of many homeowners' minds when considering tapping into their home's equity for financial needs. The time it takes to secure a home equity loan can vary significantly, influenced by a complex interplay of factors that include the borrower's financial profile, the lender's processes, and the overall state of the housing market.

Understanding the factors that affect processing times, the typical stages involved, and strategies to expedite the process can empower borrowers to make informed decisions and navigate the home equity loan journey with confidence.

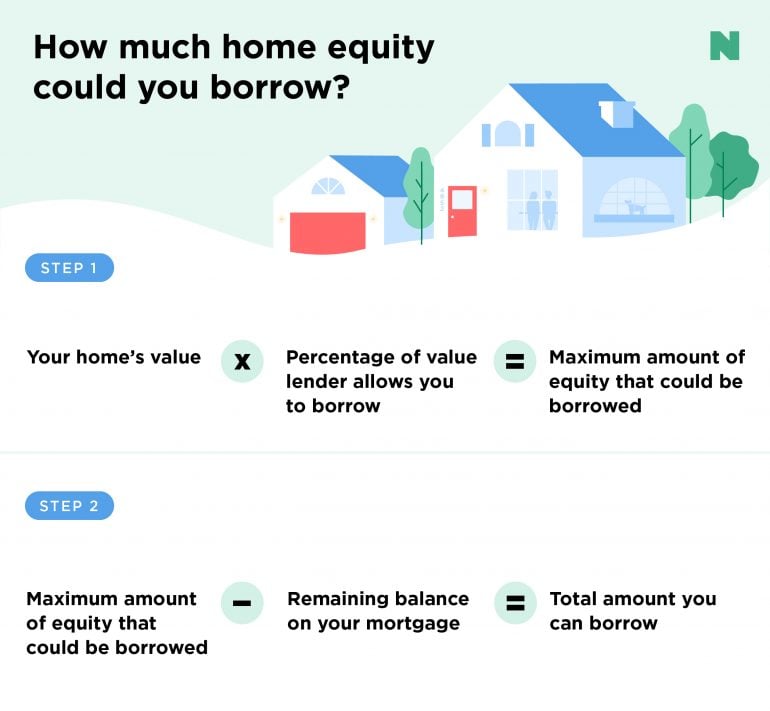

Factors Influencing Home Equity Loan Processing Time

HELOC-HomeEquity-chart.png" alt="Equity heloc loans credit" title="Equity heloc loans credit" />

The time it takes to get a home equity loan can vary significantly, depending on a number of factors. These factors can affect the speed at which lenders process your application and ultimately determine how quickly you receive the funds.

HELOC-HomeEquity-chart.png" alt="Equity heloc loans credit" title="Equity heloc loans credit" />

The time it takes to get a home equity loan can vary significantly, depending on a number of factors. These factors can affect the speed at which lenders process your application and ultimately determine how quickly you receive the funds.

Lender's Processing Time

The lender's internal processes and efficiency play a significant role in determining the processing time. Some lenders have streamlined systems and experienced staff, allowing them to process applications quickly. Others may have more complex procedures or limited resources, which can lead to longer processing times.Borrower's Financial Situation

The borrower's financial situation is a critical factor that can influence the processing time. Lenders need to thoroughly assess the borrower's credit history, income, and debt-to-income ratio to determine their ability to repay the loan. A strong credit score and stable income can expedite the process, while a poor credit history or unstable income may require additional documentation and review, leading to delays.Loan Amount and Type

The amount of the loan and the type of home equity loan requested can also impact the processing time. Larger loan amounts often require more extensive underwriting and may involve additional layers of review.For example, a home equity line of credit (HELOC) typically involves a longer processing time compared to a fixed-rate home equity loan because it requires a more complex approval process due to the revolving nature of the credit line.

Property Appraisal

A property appraisal is often required for home equity loans to determine the current market value of the property. This process can add time to the overall processing time, especially if the appraisal is delayed due to scheduling issues or if the appraiser needs to conduct additional research.Documentation and Verification

The borrower's ability to provide accurate and complete documentation is essential for a timely processing. This includes documents such as income verification, tax returns, and property deeds. Incomplete or inaccurate documentation can lead to delays as lenders need to request additional information or verify the provided details.Market Conditions

Current market conditions, such as interest rates and the overall housing market, can influence the processing time. During periods of high demand or fluctuating market conditions, lenders may experience increased application volumes, potentially leading to longer processing times.Other Factors

Other factors that can affect the processing time include the complexity of the loan terms, the borrower's location, and any special requirements or circumstances related to the loan.Typical Timeline for Home Equity Loan Processing

how long does a home equity loan take" title="Equity investments investment lendingtree" />

The processing time for a home equity loan can vary depending on several factors, including the lender, the borrower's financial situation, and the complexity of the loan. However, a typical timeline for processing a home equity loan application can be broken down into several stages, each with its own estimated timeframe.

how long does a home equity loan take" title="Equity investments investment lendingtree" />

The processing time for a home equity loan can vary depending on several factors, including the lender, the borrower's financial situation, and the complexity of the loan. However, a typical timeline for processing a home equity loan application can be broken down into several stages, each with its own estimated timeframe.

Typical Stages and Timeframes

The processing of a home equity loan application typically involves the following stages:- Application Submission and Initial Review: This stage involves the borrower submitting the loan application and providing all necessary documentation, such as proof of income, credit history, and property ownership. The lender will then review the application to ensure completeness and accuracy. This stage typically takes 1-3 business days.

- Property Appraisal and Valuation: Once the application is deemed complete, the lender will schedule a property appraisal to determine the current market value of the borrower's home. This appraisal is crucial for determining the loan-to-value (LTV) ratio, which is a key factor in loan approval. The appraisal process can take 7-14 business days.

- Loan Underwriting and Approval: After the appraisal is complete, the lender will review the borrower's financial information and credit history to assess their ability to repay the loan. This process is known as underwriting. If the borrower meets the lender's criteria, the loan will be approved. The underwriting and approval process can take 5-10 business days.

- Loan Closing and Disbursement: Once the loan is approved, the borrower will need to sign the loan documents and complete the closing process. This typically involves meeting with a loan officer to review the final loan terms and sign the necessary paperwork. After the closing is complete, the loan proceeds will be disbursed to the borrower. The closing and disbursement process can take 3-5 business days.

Typical Processing Timeline

The following table illustrates a typical timeline for processing a home equity loan application: | Stage | Estimated Timeframe | | ------------------------------------- | ------------------- | | Application Submission and Review | 1-3 business days | | Property Appraisal and Valuation | 7-14 business days | | Loan Underwriting and Approval | 5-10 business days | | Loan Closing and Disbursement | 3-5 business days | | Total Processing Time | 20-32 business days |Potential Delays in Home Equity Loan Processing

Common Reasons for Delays in Home Equity Loan Processing

Delays in home equity loan processing can arise from various factors, both internal and external to the lender.- Incomplete or inaccurate application: Missing or incorrect information on your loan application can trigger a delay as the lender needs to verify the details and ensure the accuracy of your financial profile.

- Issues with property appraisal: A property appraisal is crucial for determining the loan-to-value (LTV) ratio and ensuring the property's value justifies the loan amount. If the appraisal is delayed or results in a lower valuation than expected, it can lead to a delay in loan approval.

- Credit score fluctuations: Your credit score plays a significant role in loan approval and interest rates. Any significant changes in your credit score, such as new credit inquiries or missed payments, can impact the lender's assessment and cause a delay.

- Verification of income and employment: Lenders need to verify your income and employment to ensure you can afford the loan payments. If there are discrepancies or delays in the verification process, it can affect the loan processing time.

- Underwriting review: The underwriting process involves a thorough review of your financial information, credit history, and property details. This can be a time-consuming process, especially if there are complex factors to consider or if the lender needs to request additional information.

- External factors: External factors, such as natural disasters, economic downturns, or regulatory changes, can also lead to delays in loan processing.

Examples of Delays and Their Impact

- Delayed property appraisal: A shortage of qualified appraisers in the area, a complex property valuation, or unforeseen circumstances like bad weather can delay the appraisal process. This delay can affect the overall loan processing time and potentially lead to missed deadlines for your planned use of the funds.

- Changes in your financial situation: If you experience a significant change in your financial situation, such as a job loss or a change in your credit score, the lender might require a re-evaluation of your application, leading to a delay.

- Unforeseen documentation issues: Even seemingly minor documentation issues, such as missing tax forms or incorrect property titles, can cause delays as the lender needs to rectify these errors before proceeding with the loan approval.

Flowchart Illustrating Potential Delays, How long does a home equity loan take

[Insert a flowchart image here] Description of the flowchart: The flowchart begins with the application submission and branches out to various potential delays, such as incomplete application, issues with property appraisal, credit score fluctuations, income verification, and underwriting review. Each branch depicts the potential causes and consequences of the delay. The flowchart culminates in either loan approval or rejection, highlighting the impact of these delays on the loan processing timeline.Tips for Avoiding Delays: How Long Does A Home Equity Loan Take

:max_bytes(150000):strip_icc()/dotdash-mortgage-heloc-differences-Final-6e9607c933e9467ba4d676601497a330.jpg "Equity loan") Getting a home equity loan can be a complex process, and delays can occur for various reasons. However, borrowers can take proactive steps to minimize the risk of delays and ensure a smoother experience. Understanding the lender's requirements, providing accurate information, and maintaining effective communication are crucial for a timely loan approval.

Getting a home equity loan can be a complex process, and delays can occur for various reasons. However, borrowers can take proactive steps to minimize the risk of delays and ensure a smoother experience. Understanding the lender's requirements, providing accurate information, and maintaining effective communication are crucial for a timely loan approval.

Understanding Lender Requirements

It is essential to understand the lender's specific requirements and provide all necessary documentation upfront. This can significantly reduce the chances of delays caused by missing information or incomplete applications.- Review the lender's loan application checklist thoroughly and ensure you have all the required documents ready.

- Gather documents such as pay stubs, tax returns, bank statements, and proof of residence.

- Double-check the accuracy of all information provided on the application and supporting documents.

- Clarify any questions or uncertainties regarding the application process with the lender before submitting it.

Proactive Communication

Maintaining open and proactive communication with the lender throughout the loan process is essential. This includes timely responses to requests for information and updates on the status of the loan.- Respond to all lender inquiries promptly, providing all requested information in a timely manner.

- Check your email and phone messages regularly for any updates from the lender.

- Proactively contact the lender if you have any questions or concerns.

- Maintain a record of all communication with the lender, including dates, times, and content.

Preparing for Appraisal

The appraisal is a crucial step in the home equity loan process, and delays can occur if the appraisal is not completed efficiently.- Ensure your home is accessible to the appraiser during the scheduled appointment.

- Provide the appraiser with any relevant information about recent improvements or renovations to your home.

- Address any potential issues identified by the appraiser promptly to avoid delays.

Reviewing Loan Documents

Before signing any loan documents, review them carefully to ensure all information is accurate and you understand the terms and conditions of the loan.- Read through the loan agreement thoroughly and ask any questions you may have.

- Understand the interest rate, loan term, and any associated fees or charges.

- Clarify any unclear or confusing terms with the lender before signing the documents.