Home debt consolidation loans offer a potential solution for homeowners seeking to simplify their finances by combining multiple debts into a single, manageable loan. This strategy can streamline monthly payments, potentially lower interest rates, and reduce overall debt burden. However, it's crucial to understand the nuances of this approach, including the types of loans available, eligibility requirements, associated costs, and potential risks.

This comprehensive guide delves into the intricacies of home debt consolidation loans, providing insights into the process, benefits, drawbacks, and alternative options. We aim to equip readers with the knowledge necessary to make informed decisions regarding their debt management strategies.

Introduction to Home Debt Consolidation Loans

A home debt consolidation loan is a type of loan that allows you to combine multiple debts, such as credit card debt, personal loans, and medical bills, into a single loan with a lower interest rate. This can help you simplify your finances and save money on interest payments.

The main purpose of a home debt consolidation loan is to make it easier to manage your debt and reduce your monthly payments.

A home debt consolidation loan is a type of loan that allows you to combine multiple debts, such as credit card debt, personal loans, and medical bills, into a single loan with a lower interest rate. This can help you simplify your finances and save money on interest payments.

The main purpose of a home debt consolidation loan is to make it easier to manage your debt and reduce your monthly payments.

Benefits of Consolidating Home Debt

Consolidating home debt can offer several benefits, including:- Lower Interest Rates: By combining multiple debts into one loan with a lower interest rate, you can save money on interest payments over time. This is especially beneficial if you have high-interest debt, such as credit card debt.

- Simplified Payments: Instead of juggling multiple monthly payments, you only need to make one payment to your home debt consolidation loan. This can simplify your finances and make it easier to stay on top of your debt obligations.

- Improved credit score: Paying down your debt on time can improve your credit score, making it easier to qualify for future loans and credit cards with better interest rates.

- Reduced Stress: Having less debt and fewer monthly payments can reduce financial stress and provide peace of mind.

Potential Drawbacks of Home Debt Consolidation

While home debt consolidation loans offer benefits, it's essential to consider potential drawbacks:- Longer Loan Terms: Consolidating your debt into a home equity loan or line of credit can result in a longer loan term. This means you'll be paying off your debt for a longer period, potentially paying more in interest over time.

- Risk of Foreclosure: If you fail to make payments on your home debt consolidation loan, you could risk losing your home through foreclosure.

- Potential for Higher Interest Rates: Although home debt consolidation loans can offer lower interest rates, they can sometimes have higher interest rates than other types of loans, such as personal loans.

- Limited Access to Cash: If you have a home equity loan or line of credit, you may have limited access to cash in the future if you need to borrow money for other purposes.

Eligibility and Qualification Requirements

Securing a home debt consolidation loan involves meeting specific eligibility criteria. These requirements are designed to ensure that borrowers can manage the consolidated debt responsibly and are likely to repay the loan.

Securing a home debt consolidation loan involves meeting specific eligibility criteria. These requirements are designed to ensure that borrowers can manage the consolidated debt responsibly and are likely to repay the loan.

Credit Score Requirements

Lenders typically evaluate your creditworthiness based on your credit score. A strong credit score significantly improves your chances of loan approval and helps secure favorable interest rates.A credit score generally reflects your credit history, including your payment history, debt levels, and credit utilization.

- Minimum Credit Score: While minimum requirements vary depending on the lender, a credit score of at least 620 is often considered a good starting point. This score suggests a generally positive credit history and responsible financial management.

- Higher Credit Score: A credit score above 700 can make you a more attractive borrower, potentially leading to lower interest rates and better loan terms.

Debt-to-Income Ratio

Your debt-to-income ratio (DTI) represents the percentage of your monthly income that goes towards debt payments. Lenders use this ratio to assess your ability to manage additional debt.DTI is calculated by dividing your total monthly debt payments by your gross monthly income.

- Typical DTI Requirements: Lenders often prefer a DTI below 43%. A lower DTI indicates that you have more disposable income to cover your monthly expenses and debt payments.

- Improving DTI: To improve your DTI, consider reducing your existing debt or increasing your income.

Other Eligibility Factors

Beyond credit score and DTI, lenders may consider additional factors:- Employment History: A stable employment history demonstrates your ability to make consistent loan payments.

- Income Verification: Lenders may require proof of income, such as pay stubs or tax returns, to verify your financial stability.

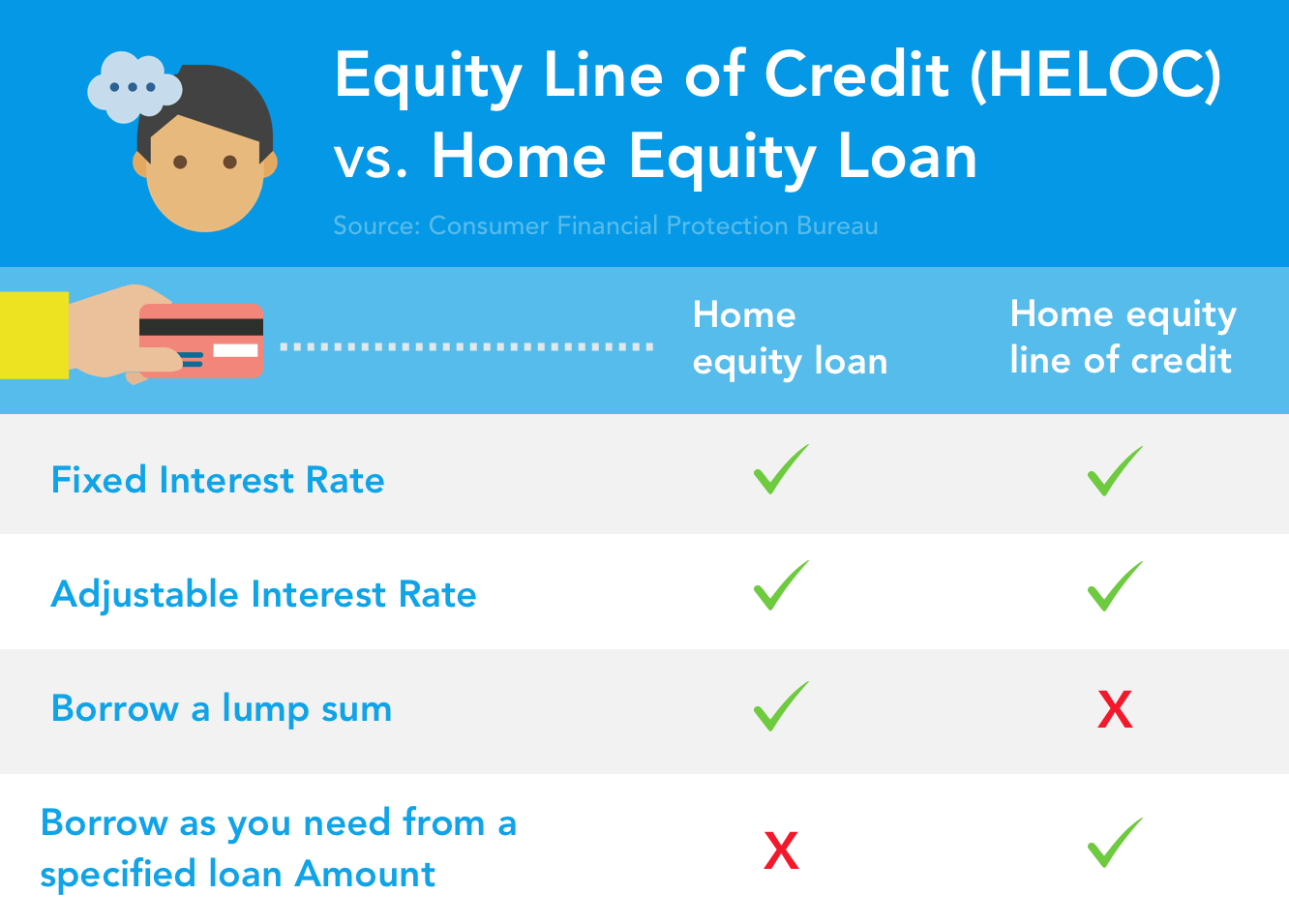

- home equity: If you're considering a home equity loan or line of credit, lenders will assess the equity you have in your home.

- Debt-to-Equity Ratio: This ratio compares your total debt to the value of your assets, including your home. A lower ratio indicates a stronger financial position.

Risks and Considerations

financing options finance using" title="Credit types cards cons pros money loans personal borrow equity debt way financing options finance using" />

While home debt consolidation loans can offer financial relief, it's crucial to acknowledge the potential risks and downsides involved. Understanding the terms and conditions of the loan, as well as potential pitfalls, can help you make an informed decision and protect yourself from financial hardship.

financing options finance using" title="Credit types cards cons pros money loans personal borrow equity debt way financing options finance using" />

While home debt consolidation loans can offer financial relief, it's crucial to acknowledge the potential risks and downsides involved. Understanding the terms and conditions of the loan, as well as potential pitfalls, can help you make an informed decision and protect yourself from financial hardship.

Understanding the Terms and Conditions

It is essential to carefully review the loan agreement and understand all the terms and conditions before signing. This includes the interest rate, loan term, fees, and any prepayment penalties.- Interest Rate: A higher interest rate can negate the benefits of consolidation and increase your overall debt burden. Compare interest rates from different lenders to find the most favorable option.

- Loan Term: A longer loan term may result in lower monthly payments but will lead to higher overall interest paid. Conversely, a shorter loan term will result in higher monthly payments but lower overall interest paid.

- Fees: Lenders often charge various fees, such as origination fees, closing costs, and prepayment penalties. These fees can significantly impact the overall cost of the loan.

- Prepayment Penalties: Some lenders impose penalties if you repay the loan early. This can deter you from paying off the loan faster and saving on interest.

Alternatives to Home Debt Consolidation: Home Debt Consolidation Loan

While home debt consolidation loans can offer a solution for managing multiple debts, it's crucial to explore alternative options that might be more suitable for your specific financial situation. These alternatives can provide flexibility and potentially lower costs compared to home equity loans.

While home debt consolidation loans can offer a solution for managing multiple debts, it's crucial to explore alternative options that might be more suitable for your specific financial situation. These alternatives can provide flexibility and potentially lower costs compared to home equity loans.

Debt Management Plans

Debt management plans, offered by non-profit credit counseling agencies, involve working with a counselor to negotiate lower interest rates and monthly payments with your creditors. This approach can help reduce your overall debt burden and improve your credit score.Pros:

- Lower monthly payments: By negotiating lower interest rates and consolidating payments, debt management plans can significantly reduce your monthly outlays.

- Improved credit score: Timely payments under a debt management plan can positively impact your credit score, making it easier to secure loans and credit in the future.

- No upfront fees: Unlike some debt consolidation options, debt management plans often do not require upfront fees.

Cons:

- Limited debt types: debt management plans typically focus on unsecured debts like credit cards and personal loans, excluding secured debts like mortgages or auto loans.

- Potential impact on credit score: While a debt management plan can ultimately improve your credit score, it may initially cause a slight dip due to the reporting of accounts in a "payment plan" status.

- Time commitment: Debt management plans can take several years to complete, requiring consistent commitment to the plan.

Balance Transfers

Balance transfers allow you to move high-interest debt from one credit card to another with a lower interest rate, typically for a promotional period. This strategy can save you money on interest charges and accelerate debt repayment.Pros:

- Lower interest rates: Balance transfers can offer significantly lower interest rates compared to your existing credit cards, reducing your overall interest costs.

- Convenience: The transfer process is usually straightforward, with many credit card issuers offering online tools for easy transfer.

- Potential for debt consolidation: Balance transfers can help you consolidate multiple credit card debts into a single account, simplifying your debt management.

Cons:

- Limited time frame: Promotional interest rates for balance transfers are typically temporary, lasting for a specific period, after which the standard interest rate applies.

- Transfer fees: Some credit card issuers charge a transfer fee, which can reduce the savings from lower interest rates.

- Credit score impact: Applying for a new credit card for a balance transfer can temporarily lower your credit score.

Debt Snowball or Avalanche Method

These methods involve prioritizing debt repayment based on either the smallest balance or the highest interest rate.Pros:

- Motivational: The snowball method, by focusing on paying off smaller debts first, provides a sense of accomplishment and momentum, encouraging continued debt repayment.

- Strategic: The avalanche method, by prioritizing debts with the highest interest rates, minimizes overall interest costs and accelerates debt reduction.

- Flexibility: Both methods offer flexibility, allowing you to adjust your repayment strategy based on your financial situation and goals.

Cons:

- Time-consuming: Both methods require consistent discipline and effort, potentially taking several years to eliminate all debts.

- Potential for setbacks: Unexpected expenses or financial emergencies can disrupt your repayment progress, potentially delaying debt elimination.

- Limited support: Unlike debt management plans, these methods do not involve professional guidance or negotiation with creditors.

Negotiating with Creditors

Directly contacting your creditors and negotiating lower interest rates, payment plans, or debt forgiveness can be a viable option, especially if you're facing financial hardship.Pros:

- Potential for significant savings: Successful negotiations can lead to lower interest rates, reduced monthly payments, or even debt forgiveness, resulting in substantial financial relief.

- Direct control: You have direct control over the negotiation process, tailoring it to your specific needs and circumstances.

- Flexibility: You can propose different negotiation options and explore various solutions that suit your financial situation.

Cons:

- Time-consuming: Negotiating with multiple creditors can be time-consuming and require persistent follow-up.

- Potential for rejection: Creditors may not be willing to negotiate, especially if you have a poor payment history.

- Lack of professional support: Negotiating with creditors on your own can be challenging, lacking the expertise and resources of a professional debt counselor.

Bankruptcy

Bankruptcy is a legal process that allows individuals to discharge or restructure their debts. It's a complex and drastic measure, typically used as a last resort when other options have been exhausted.Pros:

- Debt relief: Bankruptcy can discharge certain types of debt, providing significant financial relief and a fresh start.

- Legal protection: Filing for bankruptcy provides legal protection from creditors pursuing further collection efforts.

- Credit score impact: While bankruptcy negatively impacts your credit score, it's often a temporary setback, allowing you to rebuild your credit over time.

Cons:

- Significant financial impact: Bankruptcy can negatively impact your financial standing, potentially limiting your access to credit and future loans.

- Legal and financial complexities: Filing for bankruptcy is a complex process that requires legal expertise and careful consideration of its consequences.

- Long-term consequences: Bankruptcy can remain on your credit report for several years, potentially affecting your ability to obtain mortgages, car loans, or other financial products.

Expert Advice and Resources

Making a decision about whether or not to consolidate your home debt requires careful consideration. It's essential to weigh the potential benefits against the risks and understand the complexities involved. Seeking advice from qualified financial professionals can provide valuable insights and help you make an informed decision.Financial experts emphasize the importance of a comprehensive financial assessment before considering home debt consolidation. This involves understanding your current debt situation, income, expenses, and overall financial goals. By analyzing these factors, experts can determine if debt consolidation is the right approach for your specific circumstances.

Reputable Resources for Further Information and Guidance, Home debt consolidation loan

There are numerous reputable resources available to provide guidance and information on home debt consolidation. These resources can help you understand the process, explore different options, and make informed decisions.

- Consumer Financial Protection Bureau (CFPB): The CFPB offers comprehensive information on debt consolidation, including its potential benefits and risks. They also provide guidance on avoiding scams and protecting your rights as a consumer.

- National Foundation for Credit Counseling (NFCC): The NFCC is a non-profit organization that provides free and confidential credit counseling services. Their certified counselors can help you develop a personalized debt management plan and explore debt consolidation options.

- Financial Industry Regulatory Authority (FINRA): FINRA is a non-profit organization that regulates the securities industry. They offer resources and tools to help investors understand debt consolidation and make informed decisions.

- Local Credit Unions and Banks: Many credit unions and banks offer debt consolidation loans. It's advisable to compare rates, terms, and fees from multiple institutions before making a decision.

Seeking Professional Advice

While online resources can provide valuable information, it's highly recommended to seek professional advice from a qualified financial advisor. A financial advisor can assess your individual circumstances, provide personalized recommendations, and guide you through the debt consolidation process.

When choosing a financial advisor, ensure they are certified and have a good reputation. You can ask for referrals from trusted sources or check their credentials with regulatory bodies like the Certified Financial Planner Board of Standards (CFP Board).

"It's important to remember that debt consolidation is not a magic solution. It's a tool that can be helpful in some situations, but it's not always the best option. A financial advisor can help you determine if debt consolidation is right for you and guide you through the process." - John Doe, Certified Financial Planner