home equity loan comparison is a crucial step in the process of accessing the equity in your home for various financial needs. Whether you're planning a home renovation, consolidating debt, or simply seeking a lower interest rate, understanding the different types of home equity loans available, their terms, and the factors that influence eligibility is paramount. This guide will delve into the intricacies of home equity loans, empowering you to make informed decisions and secure the most advantageous loan for your specific circumstances.

The landscape of home equity loans is diverse, encompassing options like Home Equity Lines of Credit (HELOCs), which function like revolving credit cards, and fixed-rate loans, providing predictable monthly payments. Understanding the nuances of each type, including interest rates, APRs, repayment periods, and origination fees, is essential for comparing and selecting the loan that aligns with your financial goals and risk tolerance. Moreover, your credit score and debt-to-income ratio play a significant role in determining loan eligibility and the terms offered. This guide will equip you with the knowledge to navigate these factors and make informed decisions.

Understanding Home Equity Loans

HELOC refinance refi bursahaga" title="Equity heloc refinance refi bursahaga" />

A home equity loan, also known as a second mortgage, is a loan that allows homeowners to borrow money against the equity they have built up in their homes. Equity is the difference between the current market value of your home and the amount you still owe on your mortgage. For example, if your home is worth $300,000 and you have a mortgage balance of $150,000, you have $150,000 in equity.

Home equity loans can be a valuable financial tool for homeowners who need to access cash for various purposes. However, it's important to understand the risks and responsibilities associated with these loans before making a decision.

HELOC refinance refi bursahaga" title="Equity heloc refinance refi bursahaga" />

A home equity loan, also known as a second mortgage, is a loan that allows homeowners to borrow money against the equity they have built up in their homes. Equity is the difference between the current market value of your home and the amount you still owe on your mortgage. For example, if your home is worth $300,000 and you have a mortgage balance of $150,000, you have $150,000 in equity.

Home equity loans can be a valuable financial tool for homeowners who need to access cash for various purposes. However, it's important to understand the risks and responsibilities associated with these loans before making a decision.

Types of Home Equity Loans

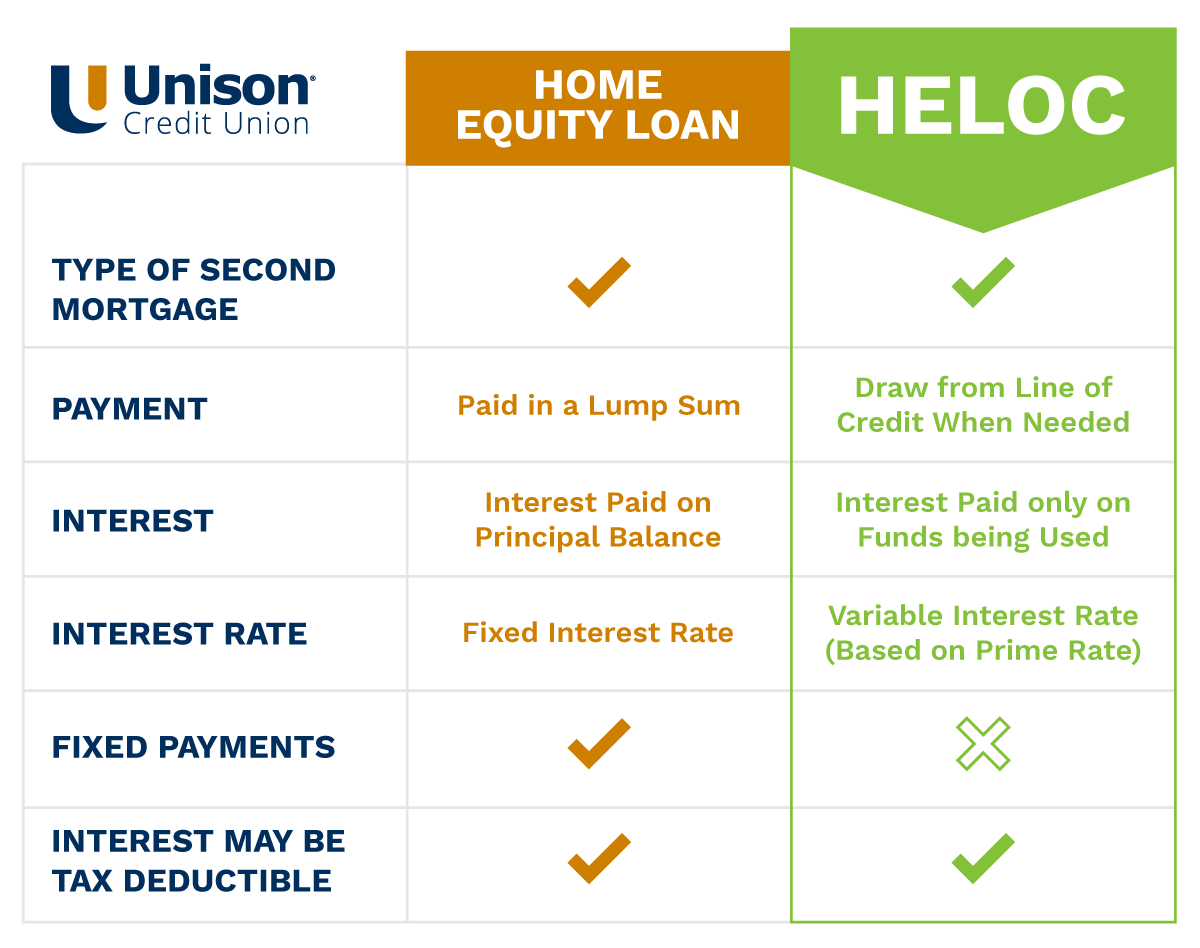

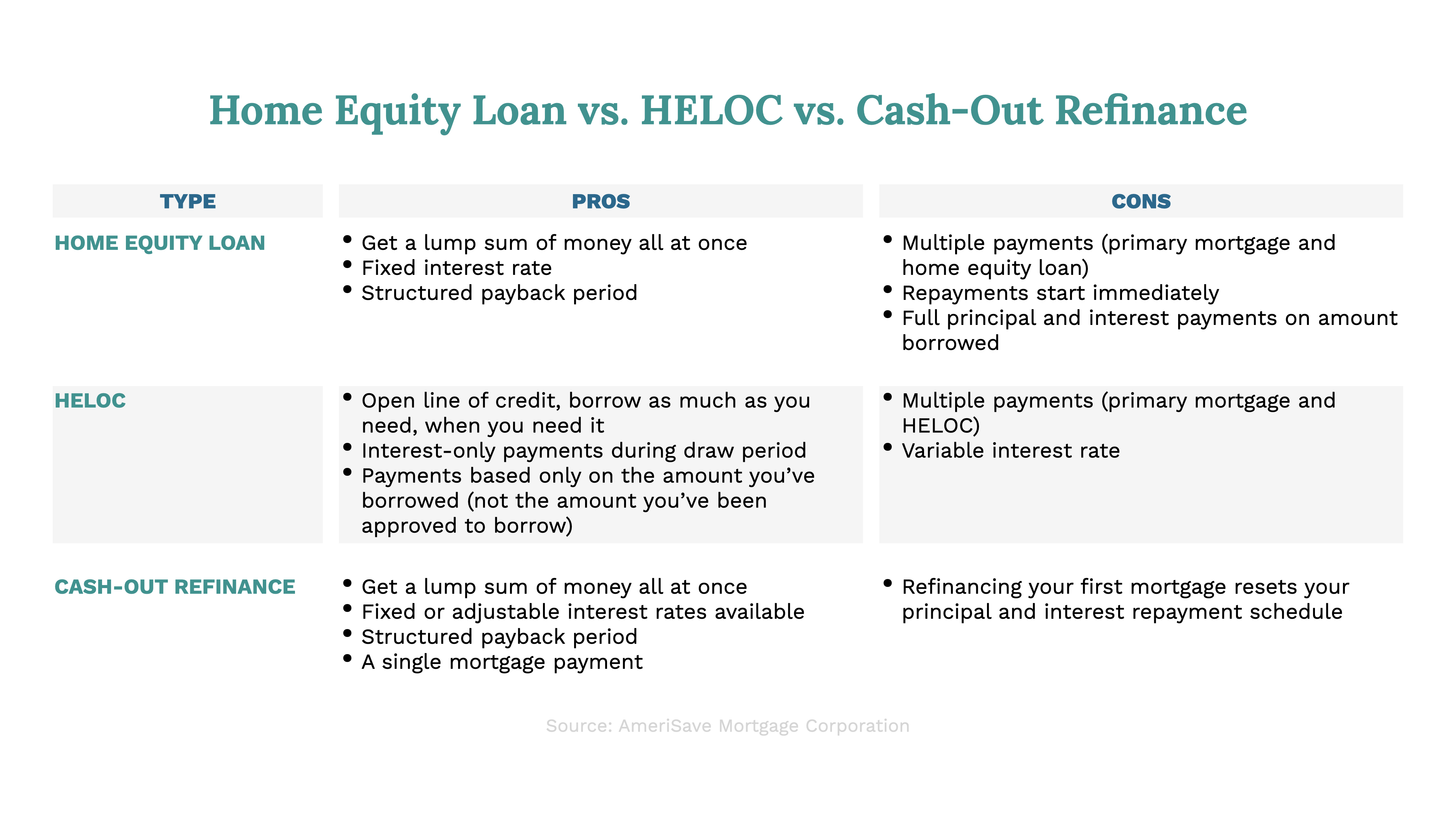

There are two main types of home equity loans:- Home Equity Line of Credit (HELOC): A HELOC is a revolving line of credit that allows you to borrow money as needed, up to a certain limit. It works similarly to a credit card, where you can draw on the credit line, make payments, and then draw on it again. HELOCs typically have variable interest rates, which means the interest rate can fluctuate over time.

- Fixed-Rate Home Equity Loan: This type of loan provides a fixed amount of money with a set interest rate that remains the same for the duration of the loan term. This offers predictability and stability in your monthly payments.

Uses of Home Equity Loans

Home equity loans are often used for various purposes, including:- Home Renovations and Improvements: Homeowners may use home equity loans to finance major renovations or improvements, such as adding a new bathroom, kitchen remodel, or finishing a basement. This can enhance the value of their homes and potentially increase their equity.

- debt consolidation: Home equity loans can be used to consolidate high-interest debt, such as credit card debt or personal loans. This can lower your monthly payments and potentially save you money on interest. However, it's important to ensure that the interest rate on the home equity loan is lower than the interest rates on your existing debts.

- Major Expenses: Homeowners may use home equity loans to finance major expenses, such as medical bills, educational costs, or unexpected emergencies.

- Investment Opportunities: In some cases, homeowners may use home equity loans to invest in opportunities, such as starting a business or purchasing rental property. However, this is a risky strategy and should be considered carefully.

Factors to Consider When Comparing Home Equity Loans: Home Equity Loan Comparison

Interest Rates and APRs

Interest rates and Annual Percentage Rates (APRs) are crucial factors to compare when evaluating home equity loans. These rates directly influence the total cost of borrowing, including both the interest charged and any additional fees. A lower interest rate generally results in lower monthly payments and a reduced overall cost.- Interest Rates: This is the percentage charged on the borrowed amount, reflecting the lender's cost of funds and risk assessment.

- APRs: APRs encompass the interest rate and additional fees, such as origination fees, mortgage insurance premiums, and closing costs. They provide a more comprehensive picture of the actual cost of borrowing.

Loan Terms

Loan terms play a crucial role in determining the repayment schedule and overall cost of a home equity loan. They specify the repayment period, the monthly payment amount, and any associated fees.- Repayment Periods: These range from a few years to as long as 30 years. Longer repayment periods typically result in lower monthly payments but higher overall interest costs. Conversely, shorter terms lead to higher monthly payments but lower overall interest costs.

- Origination Fees: These are upfront fees charged by lenders to cover the cost of processing and originating the loan. They can vary significantly among lenders and can be a substantial part of the overall loan cost.

Credit Score and Debt-to-Income Ratio, Home equity loan comparison

Your credit score and debt-to-income ratio (DTI) significantly influence your eligibility for a home equity loan and the terms you qualify for. Lenders use these metrics to assess your creditworthiness and ability to repay the loan.- Credit Score: A higher credit score typically translates into lower interest rates and more favorable loan terms. Lenders consider individuals with strong credit histories as lower risk borrowers, making them eligible for better rates.

- Debt-to-Income Ratio (DTI): This ratio represents the percentage of your monthly income that goes towards debt payments. A lower DTI indicates that you have more disposable income to make loan payments. Lenders generally prefer borrowers with a lower DTI, as it suggests a greater capacity to manage debt obligations.

Resources for Finding and Comparing Home Equity Loans

Securing a home equity loan involves researching and comparing various loan options from different lenders. Utilizing reputable resources and tools can streamline the process and ensure you find the best deal.

Securing a home equity loan involves researching and comparing various loan options from different lenders. Utilizing reputable resources and tools can streamline the process and ensure you find the best deal.

Reputable Lenders and Online Platforms

Finding the best home equity loan requires comparing offers from multiple lenders. Reputable lenders and online platforms can provide valuable resources for this process.- Banks and Credit Unions: Traditional financial institutions often offer competitive rates and terms for home equity loans. They may have local branches for in-person consultations, which can be beneficial for personalized assistance.

- Online Lenders: Online lenders can offer streamlined application processes and potentially lower rates due to reduced overhead costs. They often provide pre-qualification options, allowing you to get an idea of your potential loan terms without impacting your credit score.

- Mortgage Brokers: Mortgage brokers act as intermediaries between borrowers and lenders. They can shop around for the best rates and terms from multiple lenders, saving you time and effort.

- Comparison Websites: Websites like Bankrate, NerdWallet, and LendingTree allow you to compare rates and terms from various lenders in one place. These platforms can be helpful for quickly assessing different loan options and identifying the most competitive offers.

Using Loan Calculators and Other Tools

Loan calculators and other financial tools can help estimate monthly payments, total loan costs, and the overall impact of a home equity loan on your finances.- Loan Calculators: Online loan calculators allow you to input the loan amount, interest rate, and loan term to estimate monthly payments and total interest costs. They can also help you explore different loan scenarios and determine how changes in interest rates or loan terms affect your monthly payments.

- Debt-to-Income Ratio (DTI) Calculators: DTI calculators help determine your debt-to-income ratio, which lenders use to assess your ability to repay loans. This tool can help you understand your current financial situation and identify areas for improvement before applying for a home equity loan.

- Amortization Schedules: Amortization schedules provide a detailed breakdown of each monthly payment, including principal and interest amounts. They can help you visualize how your loan balance decreases over time and understand the overall cost of borrowing.

The Importance of Shopping Around

Shopping around and comparing offers from multiple lenders is crucial for securing the best possible terms for your home equity loan."By comparing offers from different lenders, you can potentially save thousands of dollars in interest costs over the life of your loan."

- Interest Rates: Interest rates can vary significantly among lenders. Comparing offers from multiple lenders can help you find the lowest possible rate, which can save you substantial money over the loan term.

- Loan Fees: Lenders may charge various fees associated with home equity loans, such as origination fees, appraisal fees, and closing costs. Comparing fees among lenders can help you identify the most affordable loan option.

- Loan Terms: Loan terms, such as the repayment period and prepayment penalties, can also vary among lenders. Comparing these terms can help you choose a loan that aligns with your financial goals and repayment capabilities.

Tips for Securing a Favorable Loan

mortgage loan bank cambridge" title="Heloc equity vs credit line loans mortgage loan bank cambridge" />

Securing a favorable home equity loan requires careful planning and strategic execution. By taking proactive steps to improve your creditworthiness and negotiate favorable terms, you can increase your chances of securing a loan with a competitive interest rate and minimal fees.

mortgage loan bank cambridge" title="Heloc equity vs credit line loans mortgage loan bank cambridge" />

Securing a favorable home equity loan requires careful planning and strategic execution. By taking proactive steps to improve your creditworthiness and negotiate favorable terms, you can increase your chances of securing a loan with a competitive interest rate and minimal fees.

Improving Credit Score

A strong credit score is crucial for securing a favorable home equity loan. Lenders consider your credit history as a primary indicator of your ability to repay the loan.- Pay Bills on Time: Consistent on-time payments demonstrate your financial responsibility and contribute significantly to your credit score. Late payments can negatively impact your score, making it harder to qualify for a loan or secure a favorable interest rate.

- Reduce Credit Utilization Ratio: This ratio represents the amount of credit you're using compared to your total available credit. Aim to keep your utilization ratio below 30% to improve your credit score.

- Check for Errors: Regularly review your credit report for any inaccuracies or errors that may be negatively affecting your score. You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) annually at AnnualCreditReport.com.

- Consider a Secured Credit Card: If you have limited credit history or a low credit score, a secured credit card can help build your credit. Secured cards require a security deposit, which serves as collateral for the credit line. Responsible use of a secured card can lead to improved creditworthiness over time.

Negotiating Lower Interest Rates and Fees

Negotiating a lower interest rate and fees can significantly reduce the overall cost of your home equity loan.- Shop Around: Compare offers from multiple lenders to find the most competitive rates and fees. Online comparison tools can streamline this process.

- Consider a Shorter Loan Term: A shorter loan term typically results in a higher monthly payment but a lower overall interest cost.

- Increase Your Down Payment: A larger down payment can reduce the loan amount, leading to a lower interest rate and potentially lower fees.

- Negotiate Closing Costs: Closing costs can include origination fees, appraisal fees, and other expenses. Explore options to reduce or waive these costs.

- Ask About Discounts: Some lenders offer discounts for certain borrowers, such as those with excellent credit scores, existing customers, or members of specific organizations.

Preparing for the Loan Application Process

Preparation is key to a smooth and successful loan application process.- Gather Required Documents: Be ready to provide essential documents, including your Social Security number, proof of income, bank statements, and tax returns.

- Review Your Credit Report: Before applying for a loan, check your credit report for any errors or discrepancies that could affect your eligibility or interest rate.

- Determine Your Loan Needs: Carefully consider your financial goals and determine the loan amount and repayment term that best suit your circumstances.

- Understand Loan Terms: Familiarize yourself with the terms and conditions of the loan, including interest rate, fees, and repayment schedule.